KWEB up ~20%, Comparing China vs. U.S. AI Application Playbook.

China's Open-Source Momentum Meets Super-App DNA

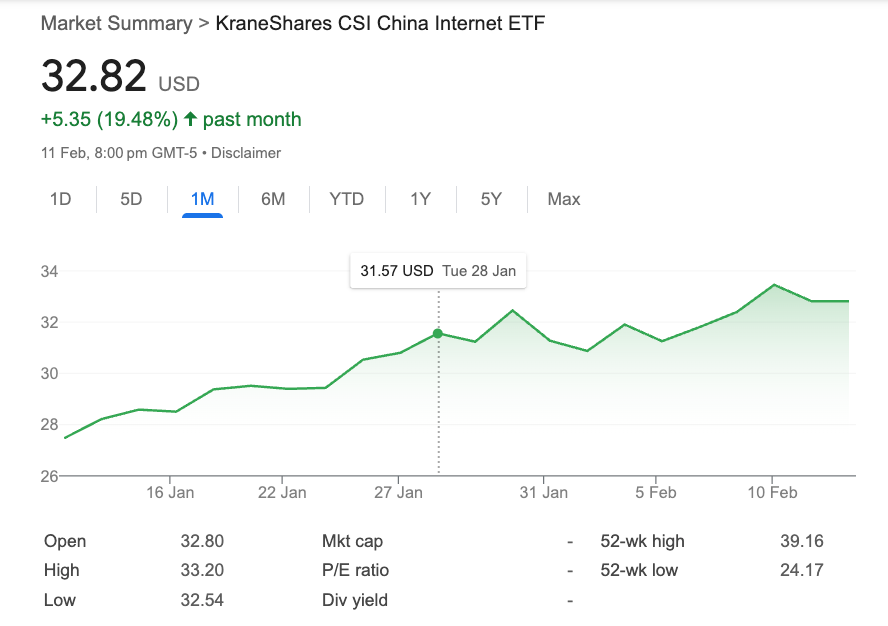

Quick mkt overview: Let’s first look at Chinese ADRs, which have risen 20 percent this month since DeepSeek’s R1 release. Investors are pricing in, and Chinese tech is apparently “investible” again. Kweb has also shot up ~20 percent since mid-January. Investment banks are sending around sales notes saying that Tencent (and Alibaba BABA 0.00%↑, Baidu BIDU 0.00%↑ ) are the “best proxy” for benefiting from the advancement of DeepSeek and Chinese AI.

TL;DR

China’s incumbent big tech have 1) access to “good enough” frontier model DeepSeek; 2) crazy amount of user data; 3) multiple touchpoints across various apps in their own ecosystems; 4) less stringent regulatory control of data sharing internally; 5) hustle work culture (unlike U.S. big tech, no one’s got time for J2, J3s, they’re all barely staying afloat in J1); 6) crazy sales force; 7) innate commercialization DNA; 8) ability to copy, copy, then innovate.

There is a chance that Chinese tech may lead in consumer-facing AI applications. I will dive deeper into the U.S.’s lead in enterprise AI application in a separate piece.

R1’s Significance to China’s AI: Open-Source Momentum

China’s LLM models have often been perceived as lagging behind U.S. giants like OpenAI, Anthropic, Meta, and Google. However, with DeepSeek’s breakthrough in the large language model, China’s AI development is finally being taken seriously by its Western peers and investors.

Many investors believe that Chinese big tech, now leaning into DeepSeek’s breakthrough with a frontier model, coupled with its innate commercial sense and competitive 996 work culture, might be able to create the next AI super app.

Meta’s Yann LeCun noted that R1’s success exemplifies the power of open-source collaboration. At this rate of adoption, it’s only a matter of months before China’s internet tech companies can combine the strength of their consumer know-how with the open-source model to accelerate AI application innovation. In fact, just yesterday, it was announced that Apple will partner up with Alibaba to develop AI features for the Chinese market.

The R1 model breakthrough represents a milestone in China's artificial intelligence landscape. As an open-source solution, R1 has quickly been adopted by China's tech giants, including Tencent, ByteDance, Huawei, and Alibaba, and integrated into their cloud infrastructure.

Recent developments in China’s AI sector have officially re-established its tech and AI capabilities on the map for global investors after a prolonged hiatus.

My point here is not that if China is to lead the innovation breakthrough in AI applications, then it is a loss for the U.S. I think it’ll just mark the start of the application hustle and the start of global consumer adoption of AI.

The West’s Shock to China’s Innovation

Fast-forward to the present. We’re at a pivotal point where value is migrating from models to applications. “China has always been very good at apps… the data, talent and capital is there,” said Alan Lau, CBO, Animoca Brands, and Vice Chairman of M+, at a HKU AI event last week.

His comment referred to the shock the West experienced at DeepSeek's success, especially the inquiries he received when attending Davos, where business leaders congregated. However, he said DeepSeek’s success, driven by domestic talent, did not surprise him at all. He believes that as value creation shifts to the application end now, China has an advantage in being the first.

China’s Super-App DNA

He recalled that in the early 2000s, when he was at Mckinsey, he would bring Chinese internet entrepreneurs to Silicon Valley to learn what they were doing. Still, by the 2010s, the tables had turned, and he was helping American entrepreneurs on tour to Shenzhen and Shanghai to learn what was happening at the frontier of tech innovation. In his eyes, China’s tech will very likely lead in application innovation.

In the most recent earnings call, Meta's CEO, Mark Zuckerberg, announced his recent vision of a “1 billion-user AI assistant” that largely hinges on Meta’s vast data and engagement. With that logic, this ambition could be applied to any of China’s tech behemoths, too.

Tencent (1.3 billion WeChat users), ByteDance (Douyin, which has 800 million DAUs), and Alibaba (over 900 million MAUs) have arguably even deeper integration into daily lives and could even tap into the data across platforms/touchpoints even easier with fewer regulatory hurdles.

China’s Multi-Modal Models

Consumer-facing AI has primarily followed a utilitarian approach in the West. ChatGPT, Perplexity, and Claude function as productivity tools—chatbots designed for research, coding, or content creation. Their interfaces are minimalistic, and their use cases are more narrowly defined. While innovative, Perplexity’s recent update for its Android assistant still prioritizes task completion: booking rides, drafting emails, or summarizing articles. This method has its advantages—85% of ChatGPT’s mobile users are male, with a significant skew toward professional use—but it risks limiting AI’s consumer use-case potential.

While Western AI tools like ChatGPT and Perplexity remain streamlined, single-purpose “answer engines,” Chinese platforms like Bytedance’s Doubao, Alibaba’s Kuake, and MiniMax’s AI suites are pioneering multi-modular interfaces that could redefine how users interact with AI and how companies monetize it.

Echoing back to China’s internet era, super-app infrastructure was widely shared to create more touchpoints for consumers and make applications feel more personalized and integrated into daily lives. This could be similar to AI applications.

Different UI/UX Preferences

In the West, we’re accustomed to minimalist app UI/UX designs. We have separate apps for each function, such as Amazon for shopping, Netflix for visual entertainment, and Spotify for music and podcasts. These tools excel at efficiency but function in silos. On the other hand, China’s mobile internet ecosystem is designed quite differently. Alibaba apps, like Taobao, feature a unique interface architecture with options for searching, purchasing, recommending, viewing videos, and using VR fitting rooms, among other things. Tencent Video boasts one of the busiest interfaces, filled with ad pop-ups, viewer commentaries, and recommendation buttons. You can even keep a virtual pet on Taobao or water virtual trees on Alipay, which can be exchanged for real tree planting by someone in the western desert regions of China if you consistently log into the app for an extended period. WeChat enables you to make video calls, voice chat, shop, pay utility bills, transfer money, and even order food or a taxi. All is to maximize touch points and engagement.

Similar trends are emerging for AI applications (see popular AI apps from China). Bytedance’s Doubao resembles a command center, featuring modular windows that serve diverse roles such as English tutor, healthcare provider, love guru, joke curator, 3D asset designer, and even a virtual Elon Musk. Each window functions as a specialized “AI agent,” with pricing tiers enabling Bytedance to monetize premium features while keeping the core query-based chatbot experience uncluttered.

While I’m not particularly fond of excessive pop-ups and multi-module features myself, I acknowledge that a more complex app with role-driven functions can enhance both business and entertainment value. When the demand for monetization arises (which it will), integrating native advertisements or paid content will likely feel much more seamless and less disruptive to the user experience in these already busy separate modules than the sleek interfaces currently provided by Western chatbots. As a regular user of apps from both universes, I can’t say one is better than the other, but if I must, Chinese mobile apps thus far have really shown creativity that is not seen in the Western ecosystem. (I.e., TikTok and RedNote that you’re now familiar with)

China’s “Copy, copy, then it flips to innovation”

Now, I don't think this divergence was accidental. In November 2024, Chinese mobile users spent an average of 7.91 hours daily on apps—mainly across the five WeChat, QQ, Douyin, Taobao, and Alipay. Compared to the U.S., where the average smartphone owner uses 10 apps per day and 30 apps each month, Chinese consumers have grown accustomed to super apps with “busy” UI/UXs that prioritize versatility over simplicity. Compared to U.S. app fragmentation, these all-in-one ecosystems (mainly due to less stringent antimonopoly laws) allow these super players to accumulate massive user bases, which they can leverage for AI apps.

Uber founder Travis Kalanick recently stated on the All-In Podcast that ten years ago, when he was trying to compete with Didi in China, he was both impressed and shocked by the speed and effectiveness of the Chinese tech company’s (Didi Chuxing) copying.

“So, but what happens is when you get really, really good at copying and that time gets tighter and tighter and tighter and tighter and tighter, you eventually run out of things to copy, and then it flips to creativity, to creativity and innovation,” said Kalanick.

But at which point does the copying turn into innovation? I think we’re starting to see that happen now in AI.

It’s the super app playbook, rooted in a decade of experimentation: make yourself indispensable and monetize at friction points.

International Investment Implications

With China’s super-app ecosystem, which presents a mosaic of touchpoints (payments, social media, e-commerce), it is clear that there is also a fertile ground for potential AI monetization.

Critics argue that China’s LLMs still trail OpenAI. But DeepSeek’s R1 model—matching GPT-o1 at a fraction of the cost—suggests the gap is closing. It’s noticeable that if China’s big tech firms are all trying to catch up to frontier LLMs, starting with Alibaba’s latest Qwen 2.5 Max, and Minimax’s Kimi K1.5, Chinese firms are pivoting to application-layer innovations, much like Tencent did with WeChat after lagging in early mobile OS wars (which was once dismissed as a WhatsApp clone).

China’s ecosystem could birth the first AI super app—a platform blending search, entertainment, commerce, and OS-like extensibility. Eventually, it will be about designing the most immersive platform the masses can use (again, for better or worse).

Ultimately, I believe the application race is not a zero-sum game. LLM incumbents like OpenAI can still maintain an advantage in their businesses across 1) model dominance, 2) top-enterprise choice API, and 3) GPT can still capture the majority of market share for the chat-bot function globally.

However, going forward, with the most frontier open-sourced models being embedded into big-tech workflows, what an AI app looks like may no longer just be in a GPT-bot form. That’s where application innovation comes in.

This essentially opens up the potential AI application market. I reiterate what Brian Wong has said here: This isn’t a win for China or a loss for the U.S. It’s a push forward for AI application innovation as a society. This means that the future AI super app, whether Chinese or American, may not matter to consumers (just as whichever model AI wrappers use also does not matter to consumer users).

Last but not least, providing some extra context: DeepSeek’s success and penetration across age groups (users under 19 to over 50) during the Lunar New Year was fueled by the right timing and some patriotic fervor domestically. What makes me think it is not just a fad but rather a signal that Chinese AI may finally be able to be a key contributor to the global innovation ecosystem is that it blew up not only in China. In fact, it topped download charts in over 140 countries within days of its launch, echoing TikTok’s global rise and highlighting a point: Consumers care less about geopolitical tensions than about accessibility, product quality, and user experience.

China’s AI and tech sector resurgence is not just about replicating U.S. models, as some would like to say, but innovating on top of them, as we saw during the internet era. DeepSeek’s founder, Liang Wenfeng, has also advocated this vision. For Chinese companies to really contribute to the global innovation ecosystem, they need to innovate in hard tech and continue to think outside the box in software (where it has the competitive advantage).

Please subscribe, share, and like if you enjoyed this analysis.

//

NEWS FLASH: **Baidu just announced they will release a next-generation model this year. **Tencent Cloud Development announced a major update on February 11, 2025, introducing a new feature that simplifies AI integration for WeChat Mini-programs. Developers can now integrate DeepSeek's large language model into WeChat Mini-programs with just 3 lines of code.

Great piece. Truly.

The main ticker for me that I follow here is $YINN. It's one of those weird x3 ETFS. It's up nearly 144% in the past year.