The WeChat Agent Dilemma — And What It Says About China's AI Endgame

Field notes from Alibaba and Tencent Cloud Summits in Hong Kong and Shanghai

Dowson Tong (汤道生) took the stage in Shanghai with a slide that showed how Tencent had mobilized from zero to a full product suite in under a week. The OpenClaw frenzy had exploded during Chinese New Year, and suddenly every product team at Tencent was racing to ship a lobster. We wrote about how Tencent led the embrace here.

But it’s been two months since that initial frenzy, now what? Why are Alibaba and Tencent throwing massive events to talk about their enterprise strategy of integrating this open-source software at their cloud summits?

Tong didn’t talk about the lobsters as a consumer product. He talked about them as the forcing function that finally made enterprises take agents seriously. How could this be an opportunity for Tencent, which has been a bit slow in AI?

“AI deployment is not just an algorithm problem. It’s an engineering problem.”

That line was the thesis of his entire keynote. And it turned out to be the thesis of both summits.

Tencent thinks it can win because it has better distribution and ecosystem than everyone else. Alibaba thinks it has a better developer ecosystem and cloud service than everyone else. Let’s rewind.

Two days earlier and a thousand kilometers away, about a hundred developers, cloud architects, and a handful of investors had gathered at the glossy space shuttle-looking office building that is supposedly the “most expensive business real estate in Hong Kong” – The Henderson, for Alibaba Cloud’s “Data+AI Forward” summit, co-hosted with AMD.

Although the target audience was much more client-facing and the discussions largely focused on data storage and add-on services offered by Alibaba, some themes were the same. It was equally about building the harness, context engineering, agent orchestration, skills marketplace, and enterprise governance.

Even MiniMax, the fast-rising model startup, appeared at both events in some capacity — at Alibaba’s stage as a case study in cross-stack data support, at Tencent as a guest speaker integrated into their TokenHub marketplace. The ecosystem is so intertwined yet so cutthroat at the same time.

What was clear was that the consumer battle was halfway done, or at least they realized that ROI is not going to be there anytime soon. As OpenClaw took off, a new wave of optimism swept through the management’s ranks. This could be an opportunity to court enterprise clients. Sell tokens? Full-stack service? Cloud, the foundation of it all.

The Consumer Party Is Over

For most of 2025, China’s AI story was a consumer story; we’ve written about it here and here. It was about capturing mindshare, super-app integrations, viral chatbots, the race for monthly active users between Doubao, Kimi, DeepSeek, and a dozen others.

Li Qiang (李强), Tencent’s Group VP and President of Government & Enterprise Business, put the scale in perspective. He started his keynote showcasing a big screen indicating that there are over six hundred million generative AI users in China, that is, every second netizen. Token prices collapsed by 99% over two years, from 50–100 RMB per million tokens to a few RMB or even cents. Daily token consumption hit 14 trillion by March 2026. These numbers cannot be ignored; they mean that, in some capacity, “AI for all” 全民AI has been achieved.

As we all know, since the start of 2026, the “AI for all” narrative has been taken to the next level, as we have seen a frenzy around claw installations. And “raising lobsters” (养虾) has become both a cultural meme and a product category. Millions of users traded deep system permissions for automated productivity. Every big tech under the sun scrambled to ship one. But the commercial lesson of that moment wasn’t about consumers. It was about their limits.

The consumer agent frenzy demonstrated that lots of people wanted agents. Nobody wanted to pay for them. Personal users will happily trade privacy for convenience, but they won’t pay enterprise prices. And open-source models have made the consumer-facing AI layer almost impossible to monetize directly — a reality that loomed over both events, even when it wasn’t spoken aloud. And the new battlefield, as Wu Yunsheng put it, was moving from AI that 'can answer' (能回答) to AI that 'can do' (能做事) — making ‘好用的AI’, AI that's actually useful."

Meanwhile, at the Alibaba summit, the recent leadership reshuffle within the Qwen team went entirely unmentioned. No one addressed what happened, why it happened, or what it means for the model roadmap. Qwen was talked about as the backdrop infrastructure support. The Qwen family was presented in its full regalia — Qwen3-Turbo, Qwen-Max, Qwen-VL, CosyVoice, and the Wan video generation suite. For a company staking its cloud growth narrative on open-source model leadership, this silence was, in its own way, a telling data point showing its strategy pivot.

The unspoken implication at both summits: open-source models are strategically essential but economically punishing in their own right. Maybe at this point, the pressure to see ROI in AI is becoming too heavy to bear.

What everyone knows is that enterprise clients are where the money has to come from. China’s internet era has always given excuses for a lack of willingness to pay. But when tokens become gas and water, and ‘AI is turned on like tap water’ as Tencent’s Li Qiang puts it, then maybe now, is when companies are going to pay, or must pay.

But my question is, why OpenCLaw now? Well, enterprise agents, governed agents, agents that live inside corporate workflows and generate cloud consumption, these are the ways Alibaba and Tencent intend to collect.

The WeChat question I have

When OpenClaw first became viral, WeChat did not integrate it. Even though it felt like Tencent led the strategic embrace and was the most hyped up about it, there was a lot of caution for WeChat, the main app at first. Allen Zhang Xiaolong (张小龙), WeChat’s legendary product manager — the person who has historically guarded the platform’s simplicity and user trust with near-religious discipline — resisted.

For him, the risks were that agents with deep system permissions operating inside WeChat’s social graph raise profound privacy, security, and compliance concerns. A misbehaving agent in a personal chat is embarrassing. A misbehaving agent in a WeChat group, one that can read messages, trigger workflows, and access contacts, is a liability at societal scale.

So what happened was that the first integration was through WeCom (企业微信), the enterprise version of WeChat. Now, this was definitely a conscious move. Enterprise use cases are more controlled — fixed user populations, IT governance, compliance frameworks, and defined workflows. An agent operating within WeCom has a bounded sandbox. The company sets permissions, the IT admin reviews skills, and the security layer audits every action. Wu Yunsheng (吴运声), speaking from the Tencent Cloud product side, laid out the enterprise security architecture in detail: four principles of agent governance — visibility (see how many agents exist), traceability (audit every action to who did what), controllability (hard limits on network and command access), and trustworthiness (security screening for every external skill). Enterprises can block agents from downloading external skills entirely, restricting them to an internal-only marketplace of vetted capabilities.

And why Allen Zhang initially withheld WeChat access.

But then Lark and DingDing integrated agents — both enterprise-first platforms with consumer-adjacent surfaces, both aggressively marketing agent capabilities. The competitive pressure became untenable, and the FOMO turned real.

If WeChat, THE platform that is Chinese digital life, didn’t offer an agent layer, it risked looking like the one platform that couldn’t do AI. But ‘doing AI’ has its risks.

So Zhang relented. Qclaw connects to WeChat via a QR code. WorkBuddy allows remote task orchestration from WeChat. But notice what is still not open: WeChat groups. (see here for more on Tencent’s claw embrace) You can invoke an agent from WeChat, but you cannot yet deploy one into a group conversation. The privacy risks and liability potential remain too high, and Zhang’s instinct and protective nature of his brainbaby WeChat, which has historically been correct, is that the downside of a social-graph agent failure far outweighs the upside of being first.

This tension that is between competitive urgency and product discipline is perhaps the most honest expression of where Chinese tech actually stands with agents. Everyone feels the pressure to push out the next ‘it’ thing, but not everyone is confident they should, or at least not test it within its products that work. If it ain’t broke, don’t fix it. right?

The Harness Thesis

Even two weeks ago, I wrote about how the biggest new buzzword in the industry feels like it’s “harness.” Tencent Dowson Tong argued at the cloud summit that as mainstream model capabilities converge — and they are converging fast, with open-source models closing the gap with proprietary ones on most benchmarks — the differentiator is no longer the model. It’s the harness, echoing what we’ve been writing about. It is the engineering scaffolding of tool calling, context management, long-term memory, and workflow design that wraps around a foundation model to make it useful in production.

This is the token refinery framework — models produce crude oil, customers pay for gasoline, and the harness is the refinery. The harness is the refinery and value migrates downstream to whoever can transform raw intelligence into something usable, trusted, and repeatable. Money moves downstream; it always does.

![[SF Part II] AI Value Captured by the Token Refineries](https://substackcdn.com/image/fetch/$s_!b46L!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fb57c5c02-5f02-464c-bdf3-a23d28d5d833_512x288.jpeg)

Tong claims that Tencent is building the best refinery. The four pillars of their Agent Core are Context Engineering, Agent Orchestration, Agent Memory, and Agent Ecosystem, which can connect to CodeBuddy on the developer side and WorkBuddy on the office-worker side, with their ADP development platform providing lifecycle management. Inside Tencent, 2,000 employees have been using WorkBuddy since January across document editing, data cleaning, and business analysis. Tasks that took hours now take twenty to thirty minutes. Token consumption keeps climbing. Tong joked that soon, employees won’t just ask their bosses for raises, but they’ll negotiate for higher monthly token budgets.

The thesis is intellectually provocative, but it raises a question that neither summit attempted to answer: if every cloud vendor is building a harness and trying to build the best refinery. The harnesses converge on the same architecture, then what exactly differentiates any of them?

Same same but different

This brings me to my final point today. I felt like everything was getting to a point where it was all a bit same-same.

For two companies with such different DNA, business models, and business units, the AI monetization logic at both events felt eerily similar.

Give enterprises agent-building tools. Those tools produce agents. Agents consume tokens. Token consumption drives cloud usage. Cloud usage drives revenue. Layer on security governance and IM distribution to make the agent sticky, and the flywheel spins. Heck, Alibaba has a new business unit helmed by its CEO Eddie Wu called the Token Hub. Meanwhile, you see below on the big screen - those big words Tencent Token Hub.

Is the thinking almost too simplistic? Integrate claw = agent tools = more agents =more token consumption = more cloud revenue.

Li Qiang was unusually candid about the fragility of this logic. He compared tokens to fuel, and that highlights the risk. As switching costs for token buyers approach zero, users switch to whoever is cheaper. I don’t care where I get my gas. I check which franchise offers me the most coupons. And he said, plainly, that Tencent would not chase token volume as a top KPI - a smart message to staff, but how are you going to make money then?

The candor laid bare the tension at the center of both companies’ strategies. If tokens aren’t the margin and models aren’t the margin, the entire enterprise bet depends on the harness layer generating enough proprietary value to justify billions in R&D. Tencent disclosed RMB 18 billion in AI spending for 2025, with further growth in 2026. Alibaba’s capex trajectory tells a similar story. But neither has yet demonstrated that agent orchestration produces sustainably differentiated revenue. For now, they are building refineries on faith.

However, if you must, underneath the convergence, there are two real strategic differences worth separating from the noise.

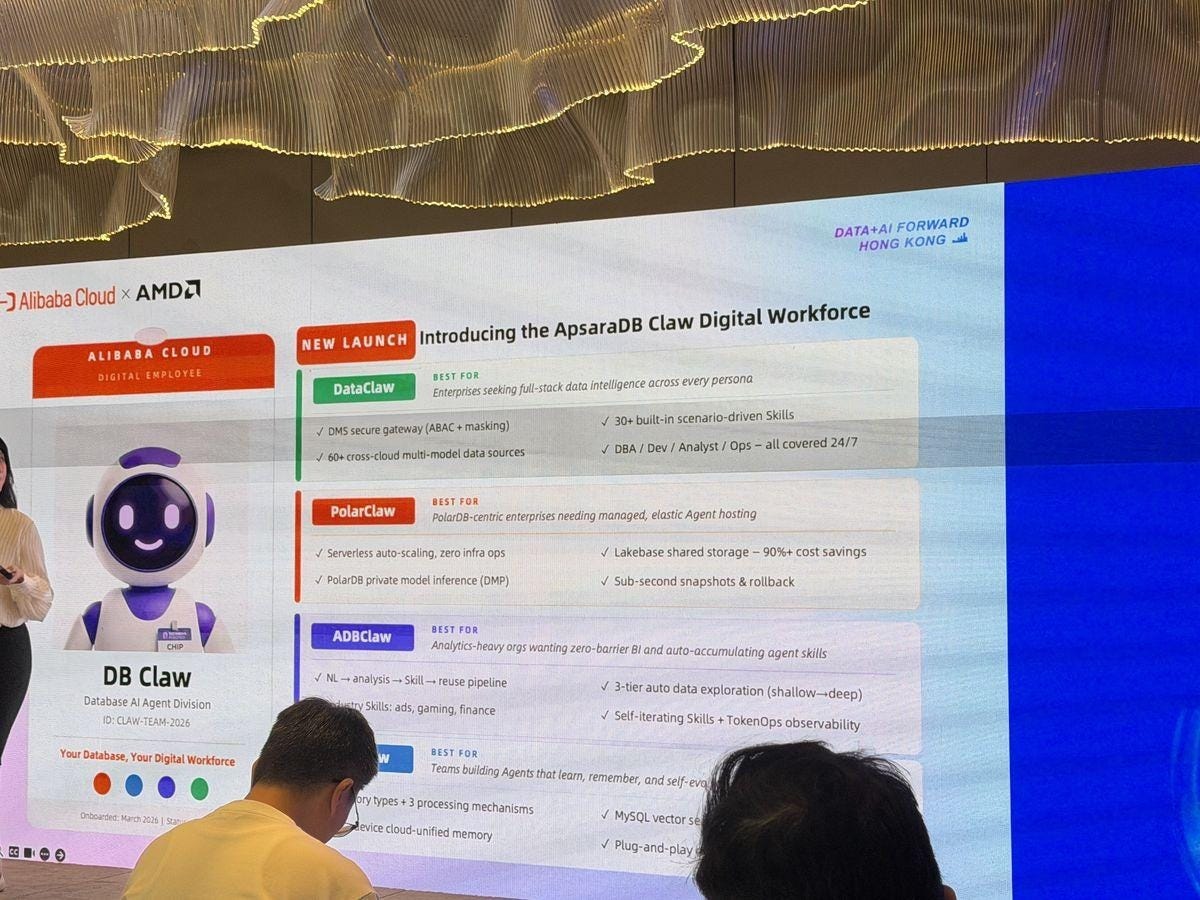

Alibaba proudly claimed that it is now the number one cloud choice for AI usage in China, and as the company expected, public cloud demand has grown as AI applications continue to find new use cases and penetrate deeper into vertical cases. Their most distinctive thesis: embed AI inference directly within the database. Enterprise data already lives in databases — a lifecycle from cold archival to warm training sets to hot production. By running the model inside the database — zero latency, data sovereignty, data gravity — the database becomes the gravitational center of the enterprise AI stack. And gravity, once established, is extremely difficult to escape. Migrating requires moving not just data, but the trained agent behaviors, skill libraries, and memory states entangled with it.

Their new ApsaraDB Claw products give this thesis a commercial form. Tbh, part of it was too technical for me. But at a high level, DataClaw, PolarClaw, and ADBClaw are agents that live where the data lives, which covers DBA, development, analytics, and operations around the clock.

In comparison, Tencent is betting on workflow embeddedness. Where Alibaba locks you in through your data, Tencent intends to lock you in through your habits. It’s probably not an exaggeration to say that WeChat is the default platform for any social interaction in China, whether enterprise use or personal use; thus, the vision, as Wu Yunsheng put it, is that AI will become like “water and electricity” as utilities, functioning in the background and turned on with a faucet, not consciously counted.

[Translation for below: Tencent strategic pyramid: Energy —> Compute —> Models —> Agents —> Applications]

So where does value accrue now?

Schumpeter observed nearly a century ago that the economic surplus from a new technology rarely accrues to its inventors. It accrues to the people who figure out how to use it. The cloud vendors are playing the role of the inventor here, building general-purpose agent infrastructure at enormous expense. But the most interesting things I saw at either summit weren’t platforms. They were the customers.

Bilibili built an AI-powered video commercialization pipeline: Qwen-Audio and Qwen-VL analyze KOL product reviews, extract brand mentions, and match them to advertiser catalogs. Bilibili's service can be very valuable because of its content taxonomy and its relationships with advertisers, which no cloud vendor can replicate.

On the Tencent side, the case study that was shared was about the Chinese Marriott, Huazhu Hotels. The hotel chain manager deployed ‘华小二’, ‘Little Hua', an AI concierge covering 152 scenarios across 38 workflow modules. For example, when a guest says, “Send me some snacks.” Within five seconds, an agent will alert the manager to dispatch the nearest staff member robot to the room. It’s now already live in over 5,000 hotels, with 94% daily usage in pilots, and is scaling to all 12,000 properties. This is again because Huazhu knows how customers behave and how to manage hotel workflows.

The model is merely an intelligence input at this point, but the industry context is the moat. If Schumpeter is right again, the billions flowing into harness layers may end up submerging the margins of the infra providers.

The bigger theme I think we can recognize is that in the cloud era, raw infrastructure has been commoditized, and the most durable value has been captured by software companies that have turned it into systems of work. In mobile, the platforms mattered enormously, but so did the companies that transformed distribution into entirely new behaviors.

In the agent era, both Alibaba and Tencent are maybe realizing that $ will not be in infra, but in the markup lives in the harness layer — the orchestration, memory, governance, and distribution scaffolding around the model. They may be right. But if the harnesses all look the same, then wouldn’t the differentiator still be in the foundation models and capabilities?

Anyway, the bet is that the value is moving one layer further out, to the companies that weave those harnesses into specific industries, specific workflows, and specific institutional contexts, no platform vendor can replicate, which, incidentally, is why vibecoding won't replace industry-specific software — context isn't something you can prompt-engineer.

I left Shanghai thinking about something Li Qiang said almost in passing. He called AI “the greatest force of certainty in an uncertain era.” That’s a good line for a keynote. But certainty about what, exactly? Will those agents exist? Sure. That those tokens be consumed? Obviously. Will the cloud vendors building all this infrastructure be the ones who profit? That part is less certain than anyone on those stages wanted to admit.

The WeChat question might be the best lens for the whole thing. Everyone knows agents need to be everywhere. Not everyone knows if letting them loose is wise. And the companies that figure out where to draw that line — in product design, in guardrails, in knowing when not to ship — might matter more than the ones that built the fastest refinery.

Great article! Regarding the shift from algorithms to engineering, this appears to be a global challenge. As model capabilities converge, the competition has shifted to scaling hardware and infrastructure. While Chinese firms may not go as all-in as their US counterparts in building massive data centers for AGI, the competitive pressure is universal. It remains to be seen how much capital these companies will ultimately commit to this infrastructure.

The concerns regarding WeChat are accurate. The app is so deeply integrated that it's used by virtually everyone in the country, very unlike users in the U.S. or Europe who might choose between Instagram, WhatsApp, or Facebook based on personal preference. In China, no substitute exists for WeChat. Because it's a private messaging tool, it contains sensitive personal and family information. Deploying Agents directly into group chats could seriously intrude on private lives. Additionally, if these Agents begin to generate spam within groups, the user experience would degrade immediately.

Thank you for sharing your perspectives. Helpful for those who are interested in China Tech but don't have the advantage of a native mandarin speaker to fully grasp what is unfolding.

On the "harness" angle, it would be nice if you can write about how Chinese firms (consumers of the harness) are hedging their bets (e.g. are they adopting both Alibaba and Tencent solutions, anything else?)